The Bootstrap Chain Ladder from Scratch using Polars

The bootstrap chain ladder from scratch using polars

Python

Actuarial

Published

January 25, 2025

In an earlier post, I provided a step-by-step guide on performing the bootstrap chain ladder using Pandas. This method involves repeatedly resampling residuals from the original chain ladder model to generate a series of simulated datasets, each replicating the original data’s claims development patterns (for more background, refer to the linked article).

Here we again walkthrough the bootstrap chain ladder step-by-step, this time using Polars, a high-performance DataFrame library built in Rust specifically designed for efficient data processing with large datasets. Unlike Pandas which is single-threaded, Polars leverages multi-core processors resulting in faster execution for many tasks. Although not required for our work in this setting, Polars can also handle datasets larger than available memory, spilling to disk when necessary. In Pandas, we can only process datasets having size less than or equal to available system memory.

Although Polars offers clear advantages over Pandas in many scenarios, this particular case isn’t one of them. Polars eliminates the concept of an index, which is a core feature of Pandas. But indices are especially valuable in this context for calculating age-to-age factors, identifying values along the latest diagonal, and squaring triangles. Additionally, while some insurers may store tens or hundreds of millions of claim records in their data warehouses, losses are typically aggregated by origin and development period ahead of a reserving analysis, resulting in datasets greatly reduced in size vs. transactional claim data. As a consequence, reserving actuaries typically don’t work with datasets large enough to necessitate parallel processing or out-of-core computation.

Translating the original Pandas bootstrap chain ladder code to Polars provided a good opportunity to showcase the library’s core features. However, many operations felt much less intuitive compared to their Pandas counterparts. Even so, I see this post as a valuable reference for specific Polars operations that I’ll likely use again in the future.

The steps to perform the bootstrap chain ladder:

Transform loss data into cumulative triangle representation.

Calculate the cumulative fitted triangle by applying backwards recursion, beginning with the observed cumulative losses from the latest diagonal.

Calculate the unscaled Pearson residuals, \(r_{p}\), degrees of freedom \(DF\) and scale parameter \(\phi\).

Calculate the adjusted Pearson residuals, defined as \(r_{p}^{{adj}} = \sqrt{\frac{n}{DF}} \times r_{p}\).

For each bootstrap sample (1…1000):

Generate a sample from the adjusted Pearson residuals \(r_{p}^{{adj}}\) with replacement.

Using the sampled adjusted Pearson residuals and fitted incremental triangle \(m\), construct the triangle of sampled incremental losses \(I_{i} = m + \hat{r}_{p}^{adj} \sqrt{m}\), where \(\hat{r}_{p}^{adj}\) represents a sample with replacement from the adjusted Pearson residuals and \(m\) the fitted incremental triangle.

Create a cumulative triangle using the result from ii., and project future losses using the chain ladder method.

Incorporate process variance by simulating each future projected incremental loss from a gamma distribution parameterized with mean equal to the projected loss value and variance the loss value times \(\phi\).

Cumulate the incremental losses, then compute the total needed reserve as the ultimate projected value minus the latest cumulative loss amount by origin period.

Compute desired quantiles of interest from predictive distribution of bootstrap samples.

In what follows each step is demonstrated, along with exhibits to visually assess the distribution of future losses.

%load_ext watermarkimport warningsimport matplotlib.pyplot as pltimport numpy as npimport pandas as pdimport polars as plnp.set_printoptions(suppress=True, precision=5)pd.set_option("display.precision", 5)pd.options.mode.chained_assignment =Nonepd.set_option('display.max_columns', None)pd.set_option('display.width', None)warnings.simplefilter(action="ignore", category=FutureWarning)pl.Config(tbl_rows=30)pl.Config(float_precision=4)pl.Config(tbl_cols=None)%watermark --python --conda --hostname --machine --iversions

Python implementation: CPython

Python version : 3.12.8

IPython version : 8.31.0

conda environment: polars

Compiler : MSC v.1942 64 bit (AMD64)

OS : Windows

Release : 11

Machine : AMD64

Processor : Intel64 Family 6 Model 170 Stepping 4, GenuineIntel

CPU cores : 22

Architecture: 64bit

Hostname: JTRIZPC11

matplotlib: 3.10.0

pandas : 2.2.3

polars : 1.20.0

numpy : 2.2.2

Start by loading the data from GitHub:

# Load RAA dataset. dfraa = pl.read_csv("https://gist.githubusercontent.com/jtrive84/976c80786a6e97cce7483e306562f85b/raw/06a5c8b1f823fbe2b6da15f90a672517fa5b4571/RAA.csv")dfraa = dfraa.sort(by=["ORIGIN", "DEV"])print("Original incremental loss data:")# Subtract 1980 from ORIGIN.dfraa = dfraa.with_columns(pl.col("ORIGIN").sub(1980).alias("ORIGIN"))dfraa.head(10)

Original incremental loss data:

shape: (10, 3)

ORIGIN

DEV

VALUE

i64

i64

i64

1

1

5012

1

2

3257

1

3

2638

1

4

898

1

5

1734

1

6

2642

1

7

1828

1

8

599

1

9

54

1

10

172

A number of functions are defined that will be used throughout the remainder of the article. Note that the implementations differ from the Pandas version: to_cum and to_incr accept an optional as_tri argument, which when set to True transforms the table of losses into a DataFrame formatted as a runoff triangle:

to_cum: Accepts an incremental loss DataFrame and returns a cumulative loss DataFrame, optionally structured as a runoff triangle.

to_incr: Accepts a cumulative loss DataFrame and returns an incremental loss DataFrame, optionally structured as a runoff triangle.

get_a2a_factors: Accepts a cumulative triangle and returns the all-year volume weighted age-to-age factors.

get_latest: Accepts a triangle and returns the value at the latest development period by origin.

square_tri: Accepts a cumulative triangle and set of age-to-age factors and projects future losses, populating the lower-right of the original cumulative triangle.

For get_a2a_factors, get_latest and square_tri, a few simplifying assumptions have been made:

The triangles under consideration have an equal number of development and origin periods.

Development periods are sequential starting with 1.

No tail factor is included.

def to_tri(df: pl.DataFrame) -> pl.DataFrame:""" Return DataFrame structured as runoff triangle. Args: df: pd.DataFrame Loss data with columns ORIGIN, DEV and VALUE. Returns: pl.DataFrame """return df.pivot(index="ORIGIN", on="DEV", values="VALUE")def to_table(tri: pl.DataFrame) -> pl.DataFrame:""" Accepts a DataFrame structured as a triangle and returns the tabular representation having columns ORIGIN, DEV and VALUE. Args: df: pd.DataFrame Loss data structures as a runoff triangle. Returns: pl.DataFrame """ df = tri.unpivot(tri.columns[1:], index=["ORIGIN"], variable_name="DEV", value_name="VALUE") df = df.with_columns(pl.col("DEV").cast(pl.Int32).alias("DEV")) df = df.sort(["ORIGIN", "DEV"])return dfdef to_cum(df: pl.DataFrame, as_tri: bool=False) -> pl.DataFrame:""" Accepts a DataFrame of incremental losses and returns a DataFrame of cumulative losses. Optionally return DataFrame as cumulative triangle. Args: df : pl.DataFrame Incremental losses. as_tri: bool Should DataFrame be returned as a triangle. Returns: pl.DataFrame """ dfc = df.with_columns( pl.col("VALUE").cum_sum().over("ORIGIN").alias("VALUE") )if as_tri:return to_tri(dfc)else:return dfcdef to_incr(df: pl.DataFrame, as_tri: bool=False) -> pl.DataFrame:""" Accepts a DataFrame with cumulative losses and de-cumulates. Args: ctri : pl.DataFrame Cumulative losses. as_tri : bool Should DataFrame be returned as a triangle. Returns: pl.DataFrame """# Get values at first development period. first_devp_values = df.filter(pl.col("DEV")==1).select("VALUE").to_numpy().flatten()# Compute difference of cumulative losses by each origin period. df = df.with_columns(VALUE=(pl.col("VALUE").diff()).over("ORIGIN"))if as_tri:# Convert to triangle. tri = to_tri(df)# Set first development period to first_devp_values. tri = tri.with_columns(pl.Series("1", first_devp_values))return trielse:return dfdef get_a2a_factors(tri: pl.DataFrame) ->list[tuple[str, float]]:""" Calculate all-year volume weighted age-to-age factors. Args: tri: pl.DataFrame Cumulative triangle. Returns: List of (age-to-age header, age-to-age factor). """ max_origin = ctri0["ORIGIN"].max() all_devps = tri.columns[1:] dps0, dps1 = all_devps[:-1], all_devps[1:] a2a_headers = [f"{ii}-{jj}"for ii, jj inzip(dps0, dps1)] a2a = []for dp0, dp1 inzip(reversed(dps0), reversed(dps1)): v1 = tri.select(str(dp0)).to_numpy().flatten()[:(max_origin -int(dp1) +1)] v2 = tri.select(str(dp1)).to_numpy().flatten()[:(max_origin -int(dp1) +1)] a2a.append((np.nansum(v2) / np.nansum(v1)).item())returnlist(zip(a2a_headers, a2a[::-1]))def get_latest(tri: pl.DataFrame) ->list[tuple[str, float]]:""" Return the value at the latest development period by origin. Args: tri : pl.DataFrame Cumulative or incremental triangle. Returns: list of (origin, latest) tuples. """if"ORIGIN"in tri.columns: tri = tri.drop("ORIGIN") nbr_devps = tri.width latest = [tri[ii, nbr_devps - ii -1] for ii inrange(nbr_devps)]returnlist(zip(tri.columns, latest))def square_tri(tri: pl.DataFrame, a2a: list[tuple[str, float]]) -> pl.DataFrame:""" Project future losses for `tri` using `a2a`. Args: tri : pl.DataFrame Cumulative triangle. a2a: list Age-to-age factors. Returns ------- pl.DataFrame Original triangle with projected future losses. """if"ORIGIN"in tri.columns: sqrd = tri.drop("ORIGIN")else: sqrd = tri _, a2a_values =zip(*a2a) nbr_devps = sqrd.widthfor r_idx inrange(nbr_devps):for c_idx inrange(nbr_devps - r_idx, nbr_devps): sqrd[r_idx, str(c_idx +1)] = sqrd[r_idx, str(c_idx)] * a2a_values[c_idx -1] sqrd = sqrd.with_row_index("ORIGIN", offset=1)return sqrd

Create an incremental loss triangle, passing dfraa into to_tri:

tri0 = to_tri(dfraa)print("Original incremental loss triangle:")tri0

Original incremental loss triangle:

shape: (10, 11)

ORIGIN

1

2

3

4

5

6

7

8

9

10

i64

i64

i64

i64

i64

i64

i64

i64

i64

i64

i64

1

5012

3257

2638

898

1734

2642

1828

599

54

172

2

106

4179

1111

5270

3116

1817

-103

673

535

null

3

3410

5582

4881

2268

2594

3479

649

603

null

null

4

5655

5900

4211

5500

2159

2658

984

null

null

null

5

1092

8473

6271

6333

3786

225

null

null

null

null

6

1513

4932

5257

1233

2917

null

null

null

null

null

7

557

3463

6926

1368

null

null

null

null

null

null

8

1351

5596

6165

null

null

null

null

null

null

null

9

3133

2262

null

null

null

null

null

null

null

null

10

2063

null

null

null

null

null

null

null

null

null

Next we create a cumulative loss triangle using to_cum with as_tri = True:

ctri0 = to_cum(dfraa, as_tri=True)print("Original cumulative loss triangle:")ctri0

Original cumulative loss triangle:

shape: (10, 11)

ORIGIN

1

2

3

4

5

6

7

8

9

10

i64

i64

i64

i64

i64

i64

i64

i64

i64

i64

i64

1

5012

8269

10907

11805

13539

16181

18009

18608

18662

18834

2

106

4285

5396

10666

13782

15599

15496

16169

16704

null

3

3410

8992

13873

16141

18735

22214

22863

23466

null

null

4

5655

11555

15766

21266

23425

26083

27067

null

null

null

5

1092

9565

15836

22169

25955

26180

null

null

null

null

6

1513

6445

11702

12935

15852

null

null

null

null

null

7

557

4020

10946

12314

null

null

null

null

null

null

8

1351

6947

13112

null

null

null

null

null

null

null

9

3133

5395

null

null

null

null

null

null

null

null

10

2063

null

null

null

null

null

null

null

null

null

Calculate the all-year volume weighted age-to-age factors

Calculate the cumulative fitted triangle by applying backwards recursion, beginning with the observed cumulative losses from the latest diagonal.

nbr_devps = ctri0.width -1a2a_headers, a2a_values =zip(*a2a)# Create empty triangle with same shape as ctri0. ctri = pl.DataFrame( {f"{i}": [np.nan] * nbr_devps for i inrange(1, 11)}).with_row_index("ORIGIN", offset=1)for r_idx inrange(ctri["ORIGIN"].shape[0]):# Determine latest development period. latest_devp = nbr_devps - r_idx# Set latest diagonal of tri to same value as in tri0. ctri[r_idx, str(latest_devp)] = ctri0[r_idx, str(latest_devp)] # Use backward recursion to un-develop triangle using a2a_values. for devp inrange(latest_devp -1, 0, -1): ctri[r_idx, str(devp)] = (ctri[r_idx, str(devp +1)] / a2a_values[devp -1])print("Fitted cumulative triangle:")ctri

Fitted cumulative triangle:

shape: (10, 11)

ORIGIN

1

2

3

4

5

6

7

8

9

10

u32

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

1

2111.3796

6332.7847

10281.4201

13066.5346

15309.7271

17045.6188

17760.4206

18351.1953

18662.0000

18834.0000

2

1889.8556

5668.3547

9202.7029

11695.6057

13703.4445

15257.2080

15897.0135

16425.8047

16704.0000

NaN

3

2699.8587

8097.8445

13147.0348

16708.4103

19576.8205

21796.5360

22710.5659

23466.0000

NaN

NaN

4

3217.7567

9651.2063

15668.9531

19913.4862

23332.1267

25977.6372

27067.0000

NaN

NaN

NaN

5

3242.8226

9726.3881

15791.0124

20068.6100

23513.8813

26180.0000

NaN

NaN

NaN

NaN

6

2186.1650

6557.0929

10645.5896

13529.3532

15852.0000

NaN

NaN

NaN

NaN

NaN

7

1989.7800

5968.0637

9689.2872

12314.0000

NaN

NaN

NaN

NaN

NaN

NaN

8

2692.6640

8076.2650

13112.0000

NaN

NaN

NaN

NaN

NaN

NaN

NaN

9

1798.7179

5395.0000

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

10

2063.0000

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

Calculate the unscaled Pearson residuals, \(r_{p}\), degrees of freedom \(DF\) and scale parameter \(\phi\).

The unscaled Pearson residuals are defined as

\[

r_{p} = \frac{I - m}{\sqrt{m}},

\]

where \(I\) represents actual incremental losses and \(m\) fitted incremental losses.

Polars doesn’t have an equivalent to Pandas df.diff(axis=1), so the implementation of to_incr is a little more involved than what we saw last post. First, the actual triangle on incremental losses:

The unscaled Pearson residuals are then calculated element-wise:

numer = tri0.select(tri0.columns[1:]) - tri.select(tri.columns[1:]) denom = tri.select(pl.col(tri0.columns[1:]).abs().sqrt())r_us = numer / denomprint("Unscaled Pearson residuals:")r_us

Unscaled Pearson residuals:

shape: (10, 10)

1

2

3

4

5

6

7

8

9

10

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

63.1259

-14.8433

-20.8573

-35.7583

-10.7510

21.7480

41.6370

0.3384

-14.5666

0.0000

-41.0341

6.5154

-40.7625

55.6209

24.7308

6.6781

-29.3664

6.2712

15.3967

null

13.6670

2.5046

-2.3670

-21.6728

-5.1237

26.7285

-8.7663

-5.5461

null

null

42.9657

-6.6508

-23.2906

19.2704

-21.5437

0.2428

-3.1923

null

null

null

-37.7697

24.7072

2.6501

31.4266

5.8049

-47.2769

null

null

null

null

-14.3973

8.4866

18.2746

-30.7401

12.3326

null

null

null

null

null

-32.1201

-8.1696

52.5357

-24.5299

null

null

null

null

null

null

-25.8555

2.8948

15.9135

null

null

null

null

null

null

null

31.4605

-22.2495

null

null

null

null

null

null

null

null

0.0000

null

null

null

null

null

null

null

null

null

\(DF = n - p\), where \(n\) is the number of populated cells in the original triangle and \(p\) the number of parameters in the chain ladder model (10 for origin period and 9 for development period):

n = tri0.count().sum().to_numpy().flatten()[1:].sum().item()p = tri0.height + tri0.width -2DF = n - pprint(f"Degrees of freedom: {DF}.")

Degrees of freedom: 36.

The scale parameter \(\phi\) is the sum of the squared unscaled Pearson residuals over the degrees of freedom:

(From this point each subsequent step is repeated up to the desired number of bootstrap samples.)

Generate a sample from the adjusted Pearson residuals with replacement:

# Set random seed for reproducibility.rng = np.random.default_rng(seed=516)# Represent adjusted residuals as Numpy array with nans and 0s removed.r = r_adj[:-1, :-1].to_numpy().flatten()r = r[np.logical_and(~np.isnan(r), r !=0)] # Sample tri0.shape[0] * tri0.shape[1] values at each iteration, but only# keep values in upper left portion of triangle. Use mask to determine # which values to retain.mask =~np.isnan(tri[:,1:])# Sample with replacement from adjusted residuals. s_r = rng.choice(r, size=mask.shape, replace=True)# # Replace 0s with nans.s_r = mask * s_rs_r[s_r==0] = np.nans_r = pl.from_numpy(s_r, schema=[str(i) for i inrange(1, 11)])print("Sample with replacement from adjusted Pearson residuals:")s_r

Sample with replacement from adjusted Pearson residuals:

shape: (10, 10)

1

2

3

4

5

6

7

8

9

10

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

-50.3838

-13.2886

7.1751

30.5389

26.8812

-18.3468

-58.4358

33.0374

10.4897

7.1751

-10.0978

8.2544

-26.7883

0.4183

78.0257

-58.4358

38.8443

-30.3197

19.6696

NaN

-27.5012

38.8443

-58.4358

-6.3330

7.1751

-27.5012

0.4183

-50.7196

NaN

NaN

-44.1984

8.0533

-37.9958

-27.5012

38.8443

-25.7803

-30.3197

NaN

NaN

NaN

19.0308

-3.9458

-26.7883

-2.9256

38.8863

7.7514

NaN

NaN

NaN

NaN

30.5681

-27.5012

26.8812

8.2544

38.8443

NaN

NaN

NaN

NaN

NaN

-39.7015

-17.7955

-18.3468

-10.8354

NaN

NaN

NaN

NaN

NaN

NaN

22.5880

-18.0048

3.0957

NaN

NaN

NaN

NaN

NaN

NaN

NaN

-25.7803

-26.7883

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

0.4183

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

Using the sampled adjusted Pearson residuals and fitted incremental triangle \(m\), construct the triangle of sampled incremental losses \({I_{i}}\):

\[

I_{i} = m + \hat{r}_{p}^{adj} \sqrt{m},

\]

where \(\hat{r}_{p}^{adj}\) represents a sample with replacement from the adjusted Pearson residuals and \(m\) the fitted incremental triangle:

tri_ii = tri[:,1:] + s_r * tri.select(pl.col(tri.columns[1:]).sqrt())tri_ii = tri_ii.with_row_index("ORIGIN", offset=1)print("Triangle of sampled incremental loss tri_ii:")tri_ii

Triangle of sampled incremental loss tri_ii:

shape: (10, 11)

ORIGIN

1

2

3

4

5

6

7

8

9

10

u32

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

1

-203.7452

3358.0144

4399.5047

4396.7778

3516.3502

971.4887

-847.5257

1393.7759

495.7340

266.1004

2

1450.8774

4285.8909

1941.7709

2513.7873

5504.0870

-749.6490

1622.3472

-168.4248

606.2675

NaN

3

1270.8943

8251.9128

896.8769

3183.4392

3252.6902

924.0302

926.6758

-638.6012

NaN

NaN

4

710.5888

7079.3951

3070.2582

2452.8309

5689.8317

1319.5115

88.6453

NaN

NaN

NaN

5

4326.5491

6165.8502

3978.4635

4086.2513

5727.7564

3066.3579

NaN

NaN

NaN

NaN

6

3615.4212

2552.7444

5807.3180

3327.0288

4194.7016

NaN

NaN

NaN

NaN

NaN

7

218.8165

2855.8569

2602.0332

2069.5944

NaN

NaN

NaN

NaN

NaN

NaN

8

3864.7765

4062.5315

5255.4183

NaN

NaN

NaN

NaN

NaN

NaN

NaN

9

705.3407

1989.8118

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

10

2081.9985

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

NaN

Create a cumulative triangle, and project future losses using the chain ladder method:

# Create cumulative triangle from sampled incremental losses.ctri_ii = to_cum(to_table(tri_ii), as_tri=True)# Get age-to-age factors for sampled cumulative triangle.a2a_ii = get_a2a_factors(ctri_ii)# Square ctri_ii, populating the lower-right side using a2a_ii.ctri_ii_sqrd = square_tri(ctri_ii, a2a_ii)print("Completed sampled triangle ctri_ii_sqrd:")ctri_ii_sqrd

Completed sampled triangle ctri_ii_sqrd:

shape: (10, 11)

ORIGIN

1

2

3

4

5

6

7

8

9

10

u32

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

1

-203.7452

3154.2692

7553.7739

11950.5517

15466.9019

16438.3906

15590.8649

16984.6408

17480.3748

17746.4752

2

1450.8774

5736.7683

7678.5392

10192.3265

15696.4135

14946.7645

16569.1116

16400.6868

17006.9544

17265.8480

3

1270.8943

9522.8071

10419.6840

13603.1232

16855.8134

17779.8436

18706.5194

18067.9182

18664.3141

18948.4374

4

710.5888

7789.9839

10860.2421

13313.0730

19002.9047

20322.4162

20411.0615

20646.5050

21328.0164

21652.6887

5

4326.5491

10492.3993

14470.8628

18557.1141

24284.8704

27351.2284

28055.8538

28379.4807

29316.2465

29762.5220

6

3615.4212

6168.1656

11975.4836

15302.5124

19497.2140

20678.4336

21211.1538

21455.8265

22164.0523

22501.4514

7

218.8165

3074.6735

5676.7067

7746.3011

10351.3688

10978.4964

11261.3256

11391.2261

11767.2341

11946.3644

8

3864.7765

7927.3080

13182.7263

17413.9552

23270.2385

24680.0431

25315.8531

25607.8739

26453.1529

26855.8442

9

705.3407

2695.1525

4093.6863

5407.6272

7226.2030

7663.9954

7861.4361

7952.1185

8214.6065

8339.6559

10

2081.9985

7378.7321

11207.6084

14804.8883

19783.7469

20982.3259

21522.8749

21771.1433

22489.7774

22832.1349

So far we’ve accounted for parameter variance, but not process variance. In order to obtain the full prediction error, we need to incorporate process variance into our estimates. This is accomplished by simulating incremental projected losses from a gamma distribution. For each cell in the lower right of the completed triangle, we randomly sample from a gamma distribution with mean equal to the projected incremental loss in that cell, and variance equal to the value in that cell times \(\phi\). For example, consider the following squared incremental triangle:

Values to the right of the main diagonal represent projected future losses. For the loss at origin = 2000 and development period = 2, the projected incremental loss is 17. We would therefore sample from a gamma distribution parameterized as follows:

from numpy.random import gamma# Computed above. phi =.798# Value at intersection of origin=2000 and development period = 2.mu =17# Determine shape and scale from mean and variance.shape = mu**2/ (phi * mu)scale = (phi * mu) / mu# Generate sample from gamma distribution.rng.gamma(shape=shape, scale=scale, size=1)# array([19.29149])

We take advantage of the fact that for the gamma distribution, the shape parameter \(\alpha = E[X]^{2} / \mathrm{Var}[X]\) and scale \(\theta = \mathrm{Var}[X] / E[X]\). In essence, we are simulating future incremental losses from a series a gamma distributions, each with parameterization based on the chain ladder-derived future incremental losses. To handle cases in which a projected incremental loss might be negative, we take the absolute value of the projected loss when determining \(\alpha_{ij}\) and \(\theta_{ij}\) for origin period \(i\), development period \(j\), where \(2 \leq i \leq n\) and \(j \geq n - i + 2\).

"""Incorporation of process variance. """from numpy.random import gamma# Get sampled squared incremental triangle.tri_ii_sqrd = to_incr(to_table(ctri_ii_sqrd), as_tri=True).drop("ORIGIN")for r_idx inrange(nbr_devps):for c_idx inrange(nbr_devps - r_idx, nbr_devps):# Get mean and variance using incremental loss value. m = np.abs(tri_ii_sqrd[r_idx, str(c_idx)]) v = m * phi# Determine shape and scale parameters. shape = m**2/ v scale = v / m# Update value at [r_idx, c_idx] with sample from gamma distribution. tri_ii_sqrd[r_idx, str(c_idx)] = rng.gamma(shape=shape, scale=scale, size=1).item()print("Sampled incremental triangle w/ process variance:")tri_ii_sqrd

Sampled incremental triangle w/ process variance:

shape: (10, 10)

1

2

3

4

5

6

7

8

9

10

f64

f64

f64

f64

f64

f64

f64

f64

f64

f64

-203.7452

3358.0144

4399.5047

4396.7778

3516.3502

971.4887

-847.5257

1393.7759

495.7340

266.1004

1450.8774

4285.8909

1941.7709

2513.7873

5504.0870

-749.6490

1622.3472

-168.4248

5.6818

258.8936

1270.8943

8251.9128

896.8769

3183.4392

3252.6902

924.0302

926.6758

261.2162

45.4568

284.1233

710.5888

7079.3951

3070.2582

2452.8309

5689.8317

1319.5115

0.0000

1187.7049

138.5052

324.6723

4326.5491

6165.8502

3978.4635

4086.2513

5727.7564

2287.3879

375.7417

20.5246

624.2870

446.2756

3615.4212

2552.7444

5807.3180

3327.0288

3960.9182

218.8131

10.1640

14.2730

306.6162

337.3991

218.8165

2855.8569

2602.0332

1195.7353

962.9821

160.2781

418.3009

0.0000

14.9545

179.1303

3864.7765

4062.5315

8917.8595

1226.2463

3936.2469

2824.7474

827.3206

4.3581

84.7208

402.6913

705.3407

1146.8776

1215.0414

619.7826

3797.3911

796.3057

8.3274

2.0791

0.2504

125.0494

2713.2565

3260.8427

1892.6994

2777.3152

1124.3156

720.6907

10.0764

7.8274

299.7176

342.3576

From this point, we proceed exactly as if performing a standard chain ladder analysis: Cumulate incremental losses, then compute the total needed reserve as the ultimate projected value minus the latest cumulative loss amount by origin period. In the next cell we convert latest_values to a numpy array to simplify differencing with ultimates, but this can also be computed element-wise in a list comprehension:

The preceding steps are repeated for the desired number of bootstrap samples, resulting in the predictive distribution of total needed reserve by origin period and in aggregate.

Bringing it All Together

The steps outlined above are combined in the next cell to run 1000 bootstrap iterations, generating the predictive distribution of reserves. We also present code to visualize the predictive distribution by origin period and in aggregate.

import matplotlib.pyplot as pltimport numpy as npfrom numpy.random import gammaimport polars as plnp.set_printoptions(suppress=True, precision=5)pl.Config(tbl_rows=30)pl.Config(float_precision=4)pl.Config(tbl_cols=None)# Set random seed for reproducibility.rng = np.random.default_rng(seed=516)# Number of bootstrap samples.nbr_samples =1000# Load tabular incremental losses. Convert to incremental triangle. dfraa = pl.read_csv("https://gist.githubusercontent.com/jtrive84/976c80786a6e97cce7483e306562f85b/raw/06a5c8b1f823fbe2b6da15f90a672517fa5b4571/RAA.csv")dfraa = dfraa.sort(by=["ORIGIN", "DEV"])dfraa = dfraa.with_columns(pl.col("ORIGIN").sub(1980).alias("ORIGIN"))tri0 = to_tri(dfraa)nbr_devps = tri0.width -1mask =~np.isnan(tri0[:,1:])# Create cumulative triangle from original losses.ctri0 = to_cum(dfraa, as_tri=True)# All-year volume-weighted age-to-age factors.a2a = get_a2a_factors(ctri0)# Cumulative fitted triangle via backwards recursion.a2a_headers, a2a_values =zip(*a2a)# Create empty triangle with same shape as ctri0. ctri = pl.DataFrame( {f"{i}": [np.nan] * nbr_devps for i inrange(1, 11)}).with_row_index("ORIGIN", offset=1)for r_idx inrange(ctri["ORIGIN"].shape[0]):# Determine latest development period. latest_devp = nbr_devps - r_idx# Set latest diagonal of tri to same value as in tri0. ctri[r_idx, str(latest_devp)] = ctri0[r_idx, str(latest_devp)] # Use backward recursion to un-develop triangle using a2a_values. for devp inrange(latest_devp -1, 0, -1): ctri[r_idx, str(devp)] = (ctri[r_idx, str(devp +1)] / a2a_values[devp -1])# Incremental fitted triangle.tri = to_incr(to_table(ctri), as_tri=True)# Unscaled Pearson residuals.numer = tri0.select(tri0.columns[1:]) - tri.select(tri.columns[1:]) denom = tri.select(pl.col(tri0.columns[1:]).abs().sqrt())r_us = numer / denom# Degrees of freedom.n = tri0.count().sum().to_numpy().flatten()[1:].sum().item()p = tri0.height + tri0.width -2DF = n - p# Scale parameter.phi = r_us.with_columns(pl.all().pow(2)).sum().to_numpy().flatten().sum().item() / DF# Adjusted Pearson residuals.r_adj = np.sqrt(n / DF).item() * r_us # Create sampling distribution from adjusted Pearson residuals. Remove# nans and 0s. r = r_adj[:-1, :-1].to_numpy().flatten()r = r[np.logical_and(~np.isnan(r), r !=0)] # Sample tri0.width * tri0.height values at each iteration, but only# keep values in upper left portion of triangle. Use mask to determine # which values to retain.sqrd_ctris = []for ii inrange(nbr_samples):# Sample with replacement from adjusted residuals. s_r = rng.choice(r, size=mask.shape, replace=True) s_r = mask * s_r s_r[s_r==0] = np.nan s_r = pl.from_numpy(s_r, schema=[str(i) for i inrange(1, 11)])# Sampled incremental triangle. tri_ii = tri[:,1:] + s_r * tri.select(pl.col(tri.columns[1:]).sqrt()) tri_ii = tri_ii.with_row_index("ORIGIN", offset=1)# Sampled cumulative triangle. ctri_ii = to_cum(to_table(tri_ii), as_tri=True)# Age-to-age factors for sampled cumulative triangle. a2a_ii = get_a2a_factors(ctri_ii)# Sampled squared cumulative triangle. ctri_ii_sqrd = square_tri(ctri_ii, a2a_ii)# Sampled squared incremental triangle. tri_ii_sqrd = to_incr(to_table(ctri_ii_sqrd), as_tri=True)# Incorporate process variance.for r_idx inrange(nbr_devps):for c_idx inrange(nbr_devps - r_idx, nbr_devps):# Get mean and variance using incremental loss value. m = np.abs(tri_ii_sqrd[r_idx, str(c_idx)]) v = m * phi# Determine shape and scale parameters. shape = m**2/ v scale = v / m# Update value at [r_idx, c_idx] with sample from gamma distribution. tri_ii_sqrd[r_idx, str(c_idx)] = rng.gamma(shape=shape, scale=scale, size=1).item() ctri_ii_sqrd2 = to_cum(to_table(tri_ii_sqrd), as_tri=True)# Keep Sampled squared triangle. sqrd_ctris.append(ctri_ii_sqrd2)

Obtain the predictive distribution of reserves and ultimates from sqrd_ctris. Each triangle in sqrd_ctris is converted to a Pandas DataFrame to keep the visualization code consistent with the prior post:

Using dfults and dfibnr, we create a summary of mean ultimate, mean IBNR, standard error of IBNR as well as 75th and 95th percentiles of the predictive distribution of reserves:

from functools importreduce# Latest cumulative loss amount by origin.latest_origin, latest_values =zip(*get_latest(ctri0))latest = ( pd.Series(data=latest_values, index=[int(ii) for ii in latest_origin]) .to_frame() .reset_index(drop=False) .rename({"index": "origin", 0: "latest"}, axis=1))# Mean ultimate by origin.ult_mean = ( dfults.groupby("origin")["ult"].mean() .to_frame() .reset_index(drop=False) .rename({"ult": "ult_mean"}, axis=1))ibnr_mean = ( dfibnr.groupby("origin")["ibnr"].mean() .to_frame() .reset_index(drop=False) .rename({"ibnr": "ibnr_mean"}, axis=1))# Standard error of reserve distribution by origin. ibnr_se = ( dfibnr.groupby("origin")["ibnr"].std(ddof=1) .to_frame() .reset_index(drop=False) .rename({"ibnr": "ibnr_se"}, axis=1))# 75th percentile of reserve distribution by origin. ibnr_75 = ( dfibnr.groupby("origin")["ibnr"].quantile(.75) .to_frame() .reset_index(drop=False) .rename({"ibnr": "ibnr_75th"}, axis=1))# 95th percentile of reserve distribution by origin. ibnr_95 = ( dfibnr.groupby("origin")["ibnr"].quantile(.95) .to_frame() .reset_index(drop=False) .rename({"ibnr": "ibnr_95th"}, axis=1))# Combine into a single DataFrame.bcl_summary =reduce(lambda df1, df2: df1.merge(df2, on="origin", how="left"), (latest, ult_mean, ibnr_mean, ibnr_se, ibnr_75, ibnr_95))# Set ult_mean for earliest origin period to latest.bcl_summary.at[0, "ult_mean"] = bcl_summary.at[0, "latest"]print("Boostrap chain ladder summary by origin:")bcl_summary.round(0)

Boostrap chain ladder summary by origin:

origin

latest

ult_mean

ibnr_mean

ibnr_se

ibnr_75th

ibnr_95th

0

1

18834

18834.0

0.0

0.0

0.0

0.0

1

2

16704

17002.0

165.0

430.0

385.0

940.0

2

3

23466

24436.0

753.0

1056.0

1228.0

2719.0

3

4

27067

29034.0

1916.0

1714.0

2824.0

5079.0

4

5

26180

29014.0

2915.0

2085.0

4023.0

6865.0

5

6

15852

19656.0

3896.0

2452.0

5218.0

8692.0

6

7

12314

18031.0

5681.0

3066.0

7513.0

11501.0

7

8

13112

24818.0

11551.0

5142.0

14783.0

21143.0

8

9

5395

16291.0

10951.0

6283.0

14557.0

22634.0

9

10

2063

20003.0

17958.0

13786.0

25409.0

43653.0

While results by origin can be useful, typically actuaries are more interested in the aggregate view. To get aggregate results, we first group by simulation number, then proceed as in the prior cell:

We can visualize actuals and predictions together by origin out to ultimate with 90% prediction intervals for each forecast period. Starting with sqrd_tris, we transform the data to make it easier for plotting:

dflist = []for tri in sqrd_ctris: dftri = ( tri.to_pandas().set_index("ORIGIN") .reset_index(drop=False) .rename_axis(None, axis=1) .rename({"ORIGIN": "origin"}, axis=1) .melt(id_vars="origin", var_name="dev", value_name="bcl_value") ) dflist.append(dftri)df = pd.concat(dflist)df["dev"] = df["dev"].astype(int)df = df.sort_values(["origin", "dev"]).reset_index(drop=True)# Compute mean, 5th and 95th percentile of prediction interval for each forecast period.df = ( df .groupby(["origin", "dev"], as_index=False)["bcl_value"] .agg({"bcl_mean": lambda v: v.mean(), "bcl_95th": lambda v: v.quantile(.95),"bcl_5th": lambda v: v.quantile(.05) }))# Attach actual values from original cumulative triangle.dfctri0 = ( ctri0.to_pandas().set_index("ORIGIN") .reset_index(drop=False) .rename_axis(None, axis=1) .rename({"ORIGIN": "origin"}, axis=1) .melt(id_vars="origin", var_name="dev", value_name="actual_value"))dfctri0["dev"] = dfctri0["dev"].astype(int)df = df.merge(dfctri0, on=["origin", "dev"], how="left")# If actual_value is nan, then dev is a prediction for that origin. Otherwise# it is an actual value. df["actual_devp_ind"] = df["actual_value"].map(lambda v: 1ifnot np.isnan(v) else0)df["value"] = df.apply(lambda r: r.bcl_mean if r.actual_devp_ind==0else r.actual_value, axis=1)df.tail(10)

origin

dev

bcl_mean

bcl_95th

bcl_5th

actual_value

actual_devp_ind

value

90

10

1

2044.92690

5819.41104

2.74973

2063.0

1

2063.00000

91

10

2

6523.89949

16103.08545

101.75998

NaN

0

6523.89949

92

10

3

10661.43665

25982.44515

319.20599

NaN

0

10661.43665

93

10

4

13682.08149

32977.99907

611.55764

NaN

0

13682.08149

94

10

5

16092.90839

38453.69231

799.41542

NaN

0

16092.90839

95

10

6

17973.94826

42833.83253

934.59346

NaN

0

17973.94826

96

10

7

18718.07392

45366.39099

1007.06181

NaN

0

18718.07392

97

10

8

19360.64161

46870.52200

1052.26676

NaN

0

19360.64161

98

10

9

19813.97172

47265.73702

1067.22772

NaN

0

19813.97172

99

10

10

20003.07058

47960.10396

1225.34543

NaN

0

20003.07058

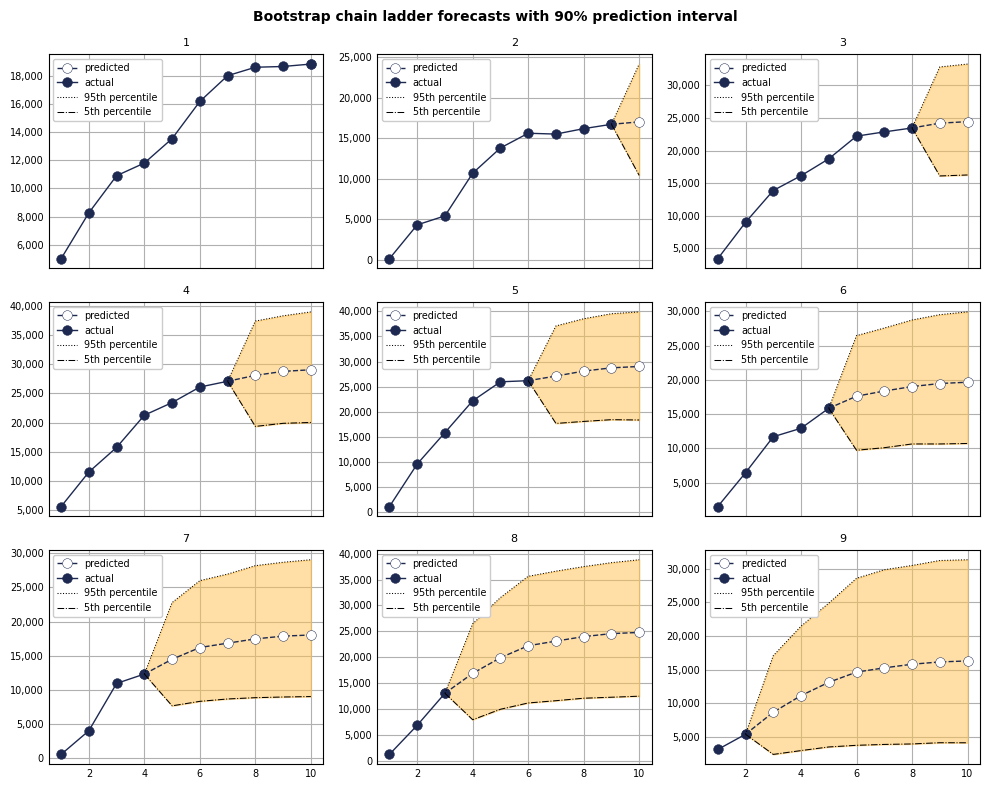

Actuals with forecasts by origin year with 90% prediction intervals:

As expected, the prediction intervals grow wider for origin periods with fewer development periods of actual data to account for the greater uncertainty in ultimate projections.

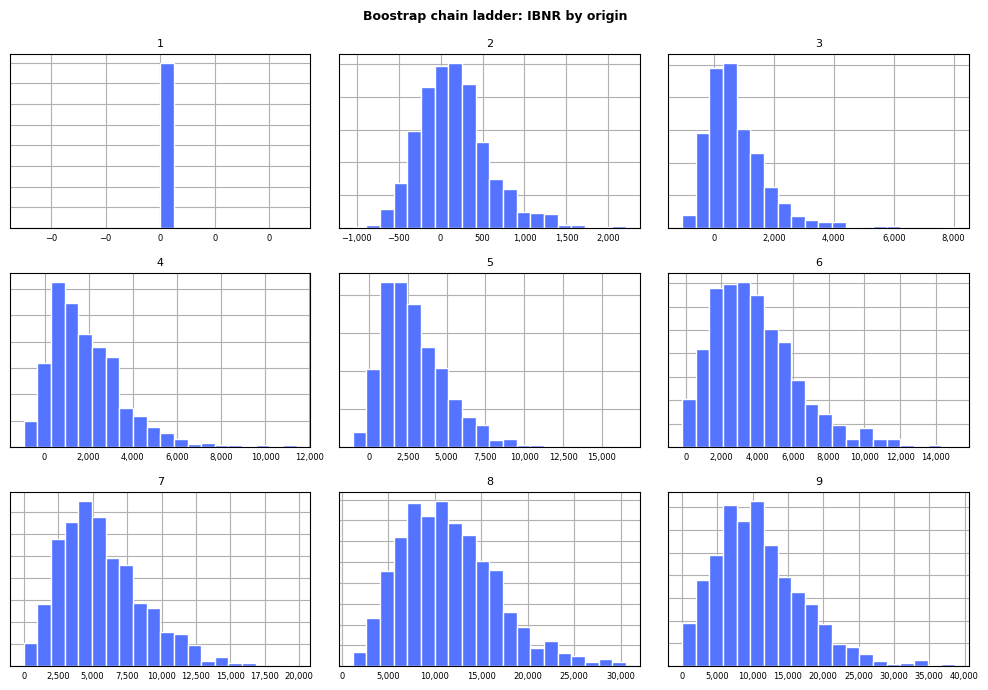

Second, an exhibit with a separate histogram per facet can be used to visualize the distribution of IBNR generated by the bootstrap chain ladder:

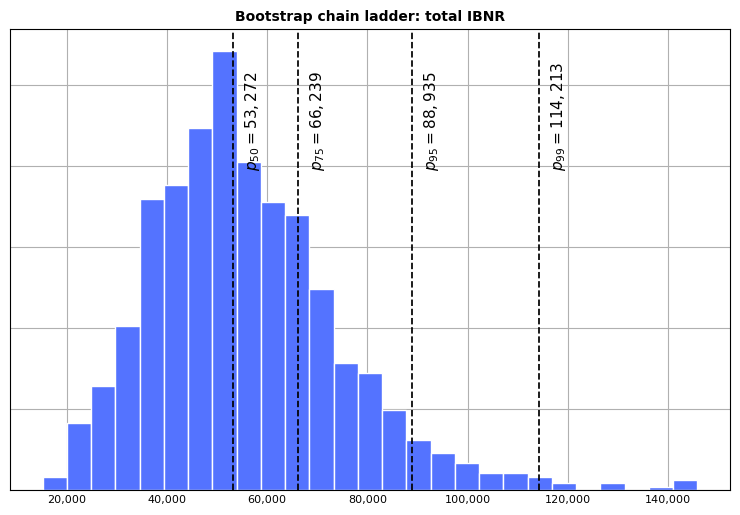

Finally, we can create a similar exhibit for the aggregate distribution of IBNR, with vertical lines added at the 50th, 75th, 95th and 99th percentile of total needed reserve: